Cruise travel insurance guide to protect your trip

Planning a cruise vacation is exciting, but medical emergencies are the most common and costly incidents at sea, with medical claims making up 27% of all cruise insurance claims. Emergency evacuations can exceed $50,000, far beyond what cruise line policies cover. Many travelers assume their cruise line insurance or credit card benefits will protect them, but coverage gaps leave thousands at risk. This guide breaks down cruise travel insurance essentials, comparing independent policies to cruise line plans, explaining what’s covered and excluded, and showing you how to choose the right protection for your vacation investment.

Table of Contents

- Key takeaways

- Why cruise travel insurance matters more than you think

- Comparing cruise line insurance vs third-party travel insurance

- How to choose the best cruise travel insurance for your trip

- Common exclusions and edge cases in cruise travel insurance

- Explore cruise deals and protect your trip with confidence

- Frequently asked questions about cruise travel insurance

Key Takeaways

| Point | Details |

|---|---|

| Independent plans offer broader coverage | Third party travel policies generally provide higher evacuation limits and broader coverage than cruise line plans. |

| High cost evacuations | Emergency medical evacuations from ships can exceed fifty thousand dollars, far above what cruise line policies typically cover. |

| Primary coverage advantage | Independent third party plans often function as primary coverage, paying claims first without waiting for your health insurer. |

| Gaps in cruise line coverage | Cruise line policies commonly have lower evacuation caps and fewer cancellation reasons compared to independent plans. |

Why cruise travel insurance matters more than you think

Cruise vacations present unique risks that standard travel insurance doesn’t always address. Medical claims dominate for cruise travelers, making up 27% of claims with average payouts increasing 14% in 2024. The confined environment, limited medical facilities, and remote locations create scenarios where minor health issues become major financial burdens.

Norovirus outbreaks alone send hundreds of passengers to ship infirmaries each year, with treatment costs ranging from $500 to $3,000 per visit. Serious conditions requiring helicopter evacuation from a ship at sea can exceed $50,000, and if you’re cruising in remote regions like Alaska or the Caribbean, those costs climb even higher. Cruise lines typically provide basic medical care onboard, but they don’t cover evacuation expenses or reimburse you for treatment costs.

Most travelers underestimate these risks because cruise vacations feel safe and controlled. The reality is different. Ships operate in international waters where your domestic health insurance provides limited or no coverage. Medicare doesn’t cover medical care outside the United States, leaving retirees particularly vulnerable. Even if your cruise line offers insurance, those policies often cap evacuation coverage at $10,000 to $30,000, a fraction of actual emergency costs.

“Emergency medical evacuations from cruise ships regularly exceed $50,000, yet many cruise line policies cap coverage at just $10,000 to $30,000, leaving travelers exposed to catastrophic out-of-pocket costs.”

Consider these specific risks that make cruise insurance essential:

- Medical emergencies requiring helicopter evacuation from ships at sea

- Norovirus or foodborne illness outbreaks requiring quarantine and treatment

- Injuries from shore excursions in countries with limited medical infrastructure

- Trip cancellations due to family emergencies, illness, or work obligations

- Missed connections causing you to miss embarkation at departure ports

- Lost or delayed baggage containing medications or essential items

Understanding cruise health and wellness tips helps you prepare, but insurance provides the financial safety net when preparation isn’t enough. The question isn’t whether you need coverage, but which type protects you best.

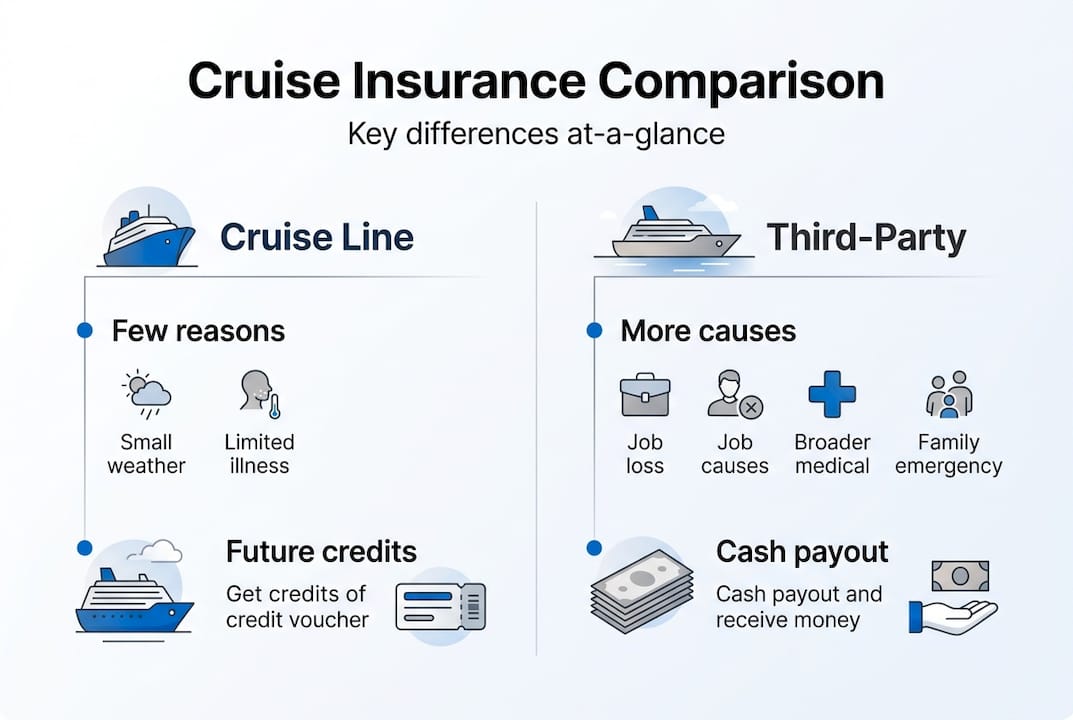

Comparing cruise line insurance vs third-party travel insurance

Choosing between cruise line insurance and independent third-party policies requires understanding fundamental differences in coverage limits, cancellation reasons, and claim flexibility. Cruise line insurance often has 10-33 times lower evacuation limits and fewer cancellation reasons compared to third-party plans. These gaps matter when you’re facing a $60,000 evacuation bill or need to cancel for a reason your cruise line policy doesn’t recognize.

Cruise line insurance is convenient because you purchase it during booking, but convenience comes with limitations. These policies typically act as secondary coverage, meaning they only pay after your primary health insurance processes claims. Third-party plans often provide primary coverage, paying claims first without requiring you to file with other insurers. This distinction saves time and hassle during emergencies when you need immediate reimbursement.

Cancellation coverage reveals the starkest differences. Cruise line policies might cover 10-15 specific cancellation reasons like serious illness or jury duty, while comprehensive third-party plans cover 25-30+ scenarios including work layoffs, home damage, and travel companion emergencies. If you need to cancel for any reason not listed, cruise line insurance won’t reimburse your prepaid expenses, but some third-party policies offer Cancel For Any Reason (CFAR) riders that reimburse 50-75% of costs.

| Feature | Cruise Line Insurance | Third-Party Insurance |

|---|---|---|

| Medical evacuation limit | $10,000 to $30,000 | $100,000 to $500,000+ |

| Medical expense coverage | $10,000 to $50,000 | $50,000 to $100,000+ |

| Cancellation reasons covered | 10-15 specific scenarios | 25-30+ comprehensive scenarios |

| Coverage type | Usually secondary | Often primary |

| Cancel For Any Reason option | Rarely available | Available as add-on (50-75% reimbursement) |

| Claim payment method | Cruise credit or voucher | Cash reimbursement |

| Cost as % of trip | 6-8% typically | 4-10% depending on coverage |

Claim payment methods also differ significantly. Cruise line insurance often reimburses cancellations with future cruise credits rather than cash refunds, locking you into rebooking with the same cruise line. Third-party plans provide cash reimbursements, giving you freedom to choose how you use refunded money. This flexibility matters if your circumstances change or you prefer a different cruise line next time.

Pro Tip: If your cruise visits remote destinations like Antarctica, Alaska, or the South Pacific, prioritize policies with at least $250,000 in evacuation coverage. These regions have limited medical facilities and require expensive long-distance evacuations that basic policies won’t fully cover.

Key differences to evaluate when comparing options:

- Primary vs secondary coverage determines whether you file with other insurers first

- Evacuation limits should match the remoteness and medical infrastructure of your destinations

- Cash reimbursements offer more flexibility than cruise credits for future bookings

- Pre-existing condition waivers vary by timing and policy requirements

Understanding these distinctions helps you make informed choices when exploring cruise booking tips and finalizing your travel protection strategy.

How to choose the best cruise travel insurance for your trip

Selecting appropriate cruise insurance requires matching coverage to your specific trip characteristics, health needs, and budget. Pre-existing condition waivers apply if insurance is purchased within 14-21 days of deposit, with look-back periods 60-120 days. This timing window is critical because missing it means pre-existing conditions won’t be covered, potentially leaving you exposed to denied claims.

Follow this step-by-step approach to identify the right policy:

- Calculate your total trip investment including cruise fare, airfare, hotels, excursions, and non-refundable deposits to determine how much coverage you need.

- Assess your health status and existing conditions to decide whether you need a pre-existing condition waiver and higher medical coverage limits.

- Evaluate your cruise destinations and determine evacuation coverage based on remoteness, with $100,000 minimum for Caribbean cruises and $250,000+ for Alaska, Antarctica, or Asia.

- Review cancellation reasons in your life circumstances, considering job security, family health, and other factors that might force cancellation.

- Compare at least three policies using comparison sites to see coverage limits, exclusions, and costs side by side.

- Purchase insurance within 14-21 days of your initial trip deposit to activate pre-existing condition waivers and early booking benefits.

Cancel For Any Reason (CFAR) coverage adds 40-60% to your base policy cost but reimburses 50-75% of trip costs if you cancel for reasons not covered by standard policies. CFAR makes sense for travelers with uncertain work schedules, aging parents, or other situations where cancellation risk is elevated. You must purchase CFAR within 14-21 days of your initial deposit and cancel at least 48 hours before departure to qualify for reimbursement.

Budgeting for cruise insurance typically means allocating 4-10% of your total trip cost. A $5,000 cruise might cost $200-$500 to insure depending on your age, trip length, and coverage level. Older travelers and those choosing comprehensive plans with high medical limits pay toward the upper end of this range. Basic plans covering only trip cancellation and minimal medical expenses cost less but leave gaps in protection.

Pro Tip: Use comparison sites like Squaremouth or InsureMyTrip to evaluate policies from multiple insurers simultaneously. These platforms let you filter by coverage type, compare evacuation limits, and read verified customer reviews to find the best value for your specific cruise.

Consider these factors when finalizing your choice:

- Trip length affects pricing, with cruises over 14 days costing more to insure

- Age significantly impacts medical coverage costs, especially for travelers over 65

- Destination remoteness should guide evacuation coverage minimums

- Pre-existing conditions require timely purchase to secure waivers

- Add-ons like CFAR or adventure sports coverage increase premiums but close protection gaps

Applying these criteria when reviewing cruise booking step by step guide resources ensures you secure appropriate protection before finalizing your cruise reservation.

Common exclusions and edge cases in cruise travel insurance

Understanding what cruise insurance doesn’t cover prevents surprises when filing claims and helps you manage expectations realistically. Policies exclude specific scenarios that travelers often assume are covered, creating gaps that leave you financially exposed if you don’t plan accordingly.

Voluntary cancellations represent the most common exclusion. If you simply change your mind or decide you don’t want to cruise anymore, no standard policy will reimburse your costs. Only CFAR coverage addresses this scenario, and even then it reimburses just 50-75% of expenses. Known events also fall outside coverage, meaning if a hurricane is already named and tracking toward your departure port when you purchase insurance, cancellations related to that storm won’t be covered.

Pandemic-related exclusions emerged prominently after 2020, with many insurers adding specific language excluding coverage for communicable disease outbreaks. Some policies now offer pandemic coverage as optional add-ons or include it in comprehensive plans, but you must verify this explicitly. Don’t assume pandemic protection is included without reading policy documents carefully.

Missed embarkation is covered if delay exceeds about 3 hours; mechanical or weather itinerary cancellations have limited coverage. If your flight delay causes you to miss your cruise departure, most policies require at least a 3-hour delay before reimbursing costs to catch up with the ship at the next port. Shorter delays typically aren’t covered, leaving you responsible for arranging and paying for transportation to meet your cruise.

| Scenario | Typically Covered? | Key Details |

|---|---|---|

| Named storm before purchase | No | Known events excluded; must buy before storm is named |

| Voluntary cancellation | No | Only CFAR covers this at 50-75% reimbursement |

| Flight delay under 3 hours | No | Most policies require 3+ hour delay for missed embarkation coverage |

| Itinerary changes by cruise line | Limited | Covers significant changes (3+ ports), not minor adjustments |

| Pre-existing conditions after deadline | No | Must purchase within 14-21 days of deposit for waiver |

| Pandemic outbreaks | Varies | Check policy; many exclude or require specific add-on |

| Adventure excursion injuries | Sometimes | Requires adventure sports rider for activities like zip-lining |

Itinerary changes present another gray area. If your cruise line alters the itinerary due to weather or mechanical issues, you’re generally not entitled to cancellation refunds unless changes are substantial. Policies typically define substantial as three or more port cancellations or a complete route change. Single port substitutions or minor timing adjustments don’t qualify for reimbursement.

Common exclusions to watch for:

- Mental health conditions unless explicitly covered in policy language

- Injuries from high-risk activities like scuba diving without proper certification

- Losses due to illegal activities or intoxication

- Cancellations due to financial circumstances like bankruptcy or job loss (unless CFAR)

- Pre-existing conditions if insurance purchased outside the waiver window

- Travel against government warnings or to restricted destinations

Mitigating these risks requires reading policy documents thoroughly before purchasing. Look for exclusion sections and ask insurers specific questions about scenarios relevant to your trip. If you’re cruising during hurricane season, confirm coverage for named storms that develop after you purchase insurance. If you have chronic health conditions, verify the pre-existing condition waiver applies to your situation.

Understanding these limitations helps you make informed decisions when exploring budget cruise booking steps guide options and selecting appropriate coverage levels for your specific circumstances.

Explore cruise deals and protect your trip with confidence

Now that you understand cruise travel insurance essentials, it’s time to put that knowledge into action by finding the perfect cruise and securing comprehensive protection. ChooseCruise makes discovering your ideal vacation simple with AI-powered recommendations, real-time price tracking, and curated deals tailored to your preferences.

Whether you’re planning a Caribbean escape, an Alaskan adventure, or a Mediterranean journey, ChooseCruise connects you with the best cruise options while helping you understand the importance of protecting your investment. Explore our platform to find & book cruise deals that match your budget and travel style, then secure insurance early to activate pre-existing condition waivers and maximize your coverage. Our cruise booking tips guide you through every step, from selecting itineraries to finalizing protection, ensuring you cruise with confidence and peace of mind.

Frequently asked questions about cruise travel insurance

Is cruise travel insurance really worth the cost?

Yes, especially given that medical emergencies make up 27% of cruise claims and evacuation costs regularly exceed $50,000. The 4-10% of trip cost you pay for comprehensive insurance protects against catastrophic financial losses that would far exceed your premium. If you’re cruising to remote destinations or have any health concerns, insurance is essential rather than optional.

When does Cancel For Any Reason coverage make sense?

CFAR coverage is worth considering if you have uncertain job security, aging parents who might need care, or other life circumstances that could force last-minute cancellation. It costs 40-60% more than standard policies but reimburses 50-75% of trip costs for any reason. You must purchase it within 14-21 days of your initial deposit and cancel at least 48 hours before departure.

What happens if I buy insurance after the pre-existing condition waiver deadline?

You’ll still have coverage for new medical issues that arise after purchasing insurance, but any pre-existing conditions won’t be covered. This means if you have diabetes, heart disease, or other chronic conditions, claims related to those conditions will be denied. The waiver deadline is typically 14-21 days after your initial trip deposit.

Am I covered if my cruise line changes the itinerary or cancels ports?

Coverage for itinerary changes is limited and typically requires substantial alterations like three or more port cancellations or a complete route change. Minor adjustments, single port substitutions, or schedule changes due to weather usually don’t qualify for reimbursement. Check your specific policy language for definitions of substantial change.

How does missed embarkation coverage work if my flight is delayed?

Most policies cover missed embarkation if your flight delay exceeds 3 hours, reimbursing costs to catch up with your ship at the next port. This includes airfare, hotels, and transportation to meet the ship. Delays under 3 hours typically aren’t covered, so build buffer time into your travel plans by arriving at your departure city at least one day early when possible.

Recommended

Related reading

6 Best Cruise Destinations 2026 for Smart First-Time Travelers

Discover the 6 best cruise destinations 2026 with expert tips for tech-savvy first-time travelers, including personalized advice for easier cruise booking.

Cruise Package Explained: Stress-Free Vacation Booking

Cruise package means bundled travel with accommodations, meals, entertainment, excursions. Learn the types, inclusions, pros, costs, and mistakes to avoid.

7 Smart Ways to Save on Cruises for Modern Travelers

Discover 7 smart ways to save on cruises with easy, practical tips designed for today’s digital cruise travelers. Learn to maximize value and minimize costs.